En

Ln

Support for High-Risk Business Models

Approved solutions for regulated, high-volume, and non-traditional industries.

Advanced Fraud & Chargeback Controls

Tools and monitoring designed to protect your account and keep it operational.

Flexible Underwriting & Scalable Limits

Structured for stability today—with room to grow responsibly.

Dedicated Support & True Partnership

Direct access to specialists who understand high-risk processing.

A high-risk merchant account is a specialized payment processing solution designed for businesses that fall outside traditional risk profiles. This classification is typically driven by factors such as industry type, transaction behavior, recurring billing models, higher average ticket sizes, or increased chargeback exposure.

Many standard processors rely on automated risk thresholds. When those thresholds are triggered, accounts are often declined, restricted, or shut down—sometimes without warning.

A properly structured high-risk merchant account uses experienced underwriting, appropriate safeguards, and the right banking relationships to ensure your business can continue accepting payments securely and compliantly.

At Data One, we believe “high risk” does not mean untrustworthy. It means your business requires expert oversight, transparency, and a payments partner built for complexity—not shortcuts.

The difference isn’t risk—it’s how that risk is managed.

OPERATION TOOLS

Whether you operate a subscription-based business, high-ticket retail model, cross-border e-commerce brand, or a regulated or high-risk industry, we structure payment solutions that are compliant, stable, and built to last.

Our team specializes in complex business models that require experienced underwriting—not automated declines.

Subscription & Recurring Billing Models

High-Ticket Retail & Wholesale Transactions

Cross-Border & International E-commerce

CBD, Hemp & Nutraceuticals* (where compliant)

Travel, Events & Ticketing

Digital Goods, Software & Online Services

Elevated Chargeback Risk Businesses

Startups & Businesses with Limited Processing History

Subject to applicable laws and banking requirements.

We deploy layered fraud prevention, real-time transaction monitoring, tokenization, and chargeback mitigation strategies—designed to protect your account and reduce disruption.

Every business is underwritten individually. Expect fair risk assessment, tailored processing limits, and clearly defined reserve structures—no automated declines or cookie-cutter decisions.

No hidden fees. No buried clauses. All pricing, reserves, and chargeback costs are clearly outlined upfront—so you know exactly how your account is structured from day one.

You’ll work with experienced specialists who understand high-risk processing—not a call center. We provide ongoing guidance through compliance, risk management, and growth.

Provide key information about your business model, products, and processing needs.

We assess risk and structure transparent, realistic terms.

Finalize contracts and complete required compliance steps.

Begin processing with ongoing support from our team.

Typical approval timelines: 3–7 business days, depending on business type and complexity.

Real-time detection and blocking of suspicious transactions.

Flexible models that adapt to your business’s cash flow and risk profile.

Early warnings and help with representment to reduce losses

For businesses selling cross-border, ensuring global cards are accepted.

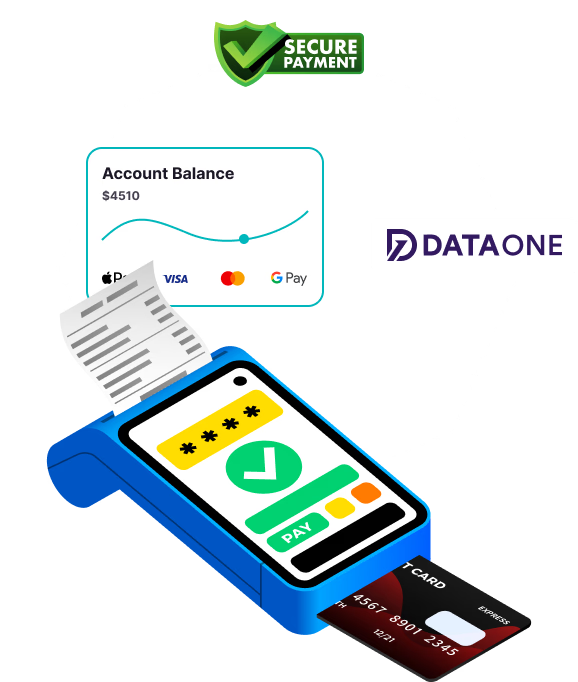

Cards, digital wallets, ACH / e-check (when relevant), recurring billing, pay-by-link, and alternative payment methods (subject to compliance).

Track sales, chargebacks, reserves, payouts — all in one place, for clarity and control.

High-risk merchant accounts operate differently than standard processing—and understanding those differences upfront is critical. Transparency around pricing, reserves, and risk controls is what allows accounts to remain stable, compliant, and operational long term.

We believe informed merchants make better partners.

Adjusted processing rates based on risk profile and industry

Rolling or fixed reserve structures, when required

Defined settlement timelines or delayed payouts in certain cases

Enhanced underwriting and compliance review

All terms are clearly disclosed before you move forward—and structured to support long-term account stability.

Retail Store Owner

Retail Store Owner

Retail Store Owner

Retail Store Owner

Retail Store Owner

Retail Store Owner

Share a few details about your business. Our underwriting team will review your model and provide a clear, transparent high-risk processing structure—no guesswork, no surprises.

FAQ

Clear answers for businesses operating in high-risk categories.

All rights reserved @ 2026